We’ve written quite a bit about where to live and how that decision relates to mortgages. See Moving Out or Best Places to Retire, for example. Well, you can pretty much scrap all of that now, thanks to corona. Holy moses--where to go, where to go?

Are big cities the place to be or not to be? Let’s look at the biggest biggie--NYC-- and the Northeast US.

America’s Big Cities were Already Losing Their Allure

Have people in big cities finally had enough?

“Todd Richardson, vice president of sales and marketing for a real estate developer in South Florida, said in recent weeks he had seen a significant jump in inquiries for a luxury condo building being built in Boca Raton, where three-bedroom units start at $1.75 million.

In the past, he said, he typically got one or two leads a day from the Northeast. 'We are right now averaging eight to 10 per day from the wealthy suburbs of New Jersey, Manhattan and Long Island,' he said, as well as other parts of the Northeast that have been hit hard by the virus. 'It’s staggering.'”

On the other hand, I have two friends from Pennsylvania who are moving to New York City. They have always wanted to live there (“... the hub of the universe! …”) and claim the time is perfect. With so many moving out, property values have dropped. People like my friends are seizing the moment to buy. There are currently several properties they told me they could not afford last year which have all dropped in price significantly. Check out this Realtor.com link to see all of the “New” listings from just the past few days!

In Home Prices Are Dropping Fast In These NYC Neighborhoods, we read that 212 homes in the Upper East Side dropped in price, including one at 834 Fifth Ave. which saw $9 million come off its price. Now there’s a bad day for a property owner! 😡 I wonder if my do-not-seem-to-be-THAT-rich friends are looking at that one.

However, that wasn’t the only part of NYC that saw a price drop. Prices went down a median of 24.9% in Midwood, Brooklyn.

So what will happen to the mortgage market with all of this (literal) movement? And what of the housing market for the remainder of 2020?

Let me veer off topic here for just a moment; yes, I will now digress. In case you are not a Facebook, Instagram, or even Twitter aficionado, the year 2020 is being called things like Satan, the Apocalypse, The Year of Insanity, etc.

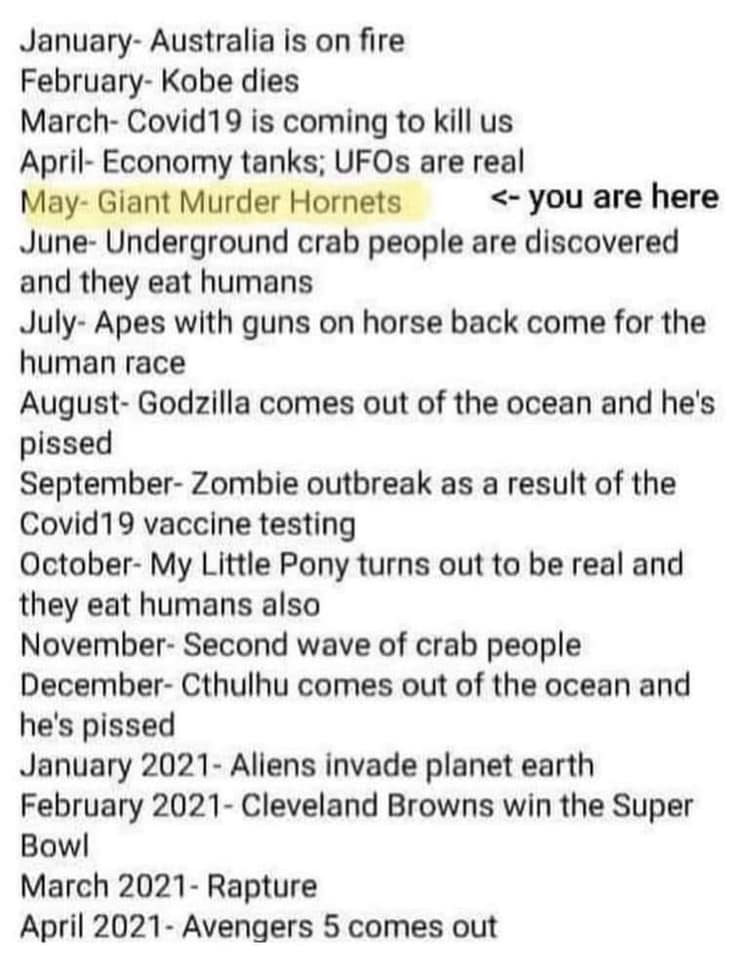

January and February were filled with news on the fires in Australia and the death of Kobe Bryant. Then March and April threw us into Covid-19 and another horrendous economy. Then the protests, riots, and sand storm started, accompanied by talks of the murder hornets. It was all a little like this May meme:

I’m typing this at the start of July. Here’s the ominous prediction for this month.

With apologies to my editor, I had to insert some humor into the middle here. I was getting depressed. And meth gators are a joke--not real. Relax everyone. However, all the rest discussed here is very real. Back on topic.

The Consumer Financial Protection Bureau (mainly from home, I presume) issued a 2 part bulletin for mortgage holders who found themselves “in trouble.” [No, they were not pregnant out of wedlock.] The new federal law applies to homeowners with federally or Government Sponsored Enterprise (GSE)-backed mortgages. It is appropriately called the Coronavirus Aid, Relief, and Economic Security (CARES) Act. And please don’t get me started on acronyms.

- First, your lender or loan servicer may not foreclose on you until at least August 31, 2020. Specifically, the CARES Act and the recent guidance from the GSEs, the FHA, the VA, and the USDA, prohibit lenders and servicers from beginning a judicial or non-judicial foreclosure against you, or from finalizing a foreclosure judgment or sale. This protection began on March 18, 2020, and extends through at least August 31, 2020.

- Second, if you experience financial hardship due to the coronavirus pandemic, you have a right to request and obtain a forbearance for up to 180 days. You also have the right to request and obtain an extension for up to another 180 days. You must contact your loan servicer to request this forbearance. There will be no additional fees, penalties or additional interest (beyond scheduled amounts) added to your account. You do not need to submit additional documentation to qualify other than your claim to have a pandemic-related financial hardship.

Great! But what happens after that? And will this affect ME?

“... because I am involved in mankind, and therefore never send to know for whom the bells tolls; it tolls for thee."

Sorry, I lapsed into a John Donne poem there. Anyway, let’s look at what the experts predict for the housing and mortgage market for the remainder of 2020.

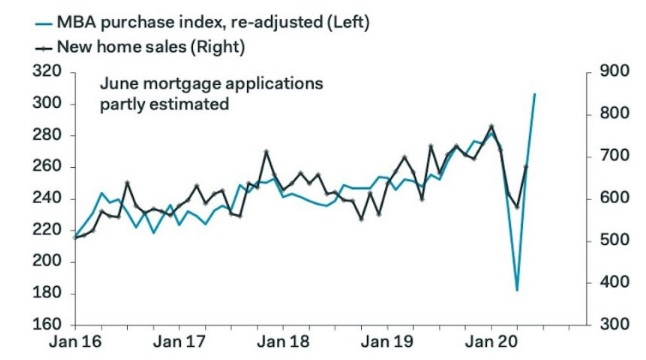

Realtor.com: Home sales are constrained by low inventory and diminished seller and buyer confidence as the effects of COVID linger in the labor market 👇

GordCollins: New home sales rose 17% last May ☝

Resale home sales dropped by 9.7% 👇

Bankrate: 8% say rates will go up

15% say rates will go down

77% say unchanged

UPI: [United Press International] U.S. mortgage applications up nearly 20 percent over 2019

I aspire to a life of positive living. As such, I am self-programmed to always find the positive in the, err, challenges life presents. Therefore, here’s what I think.

The year 2020 is providing enormous challenges for nearly every industry, home owner, world citizen, and non-murder hornet. But many, many people are buying new homes and that is spurring not just the mortgage industry, but at least 11 other lines of work: moving companies, contractors, real estate agents, landscapers, decorators, electricians, real estate attorneys, title companies, wifi providers, food stores, and furniture stores … for example. Now, take any one of those. Let’s choose electricians. In order for them to install new things in a new house a person may be moving into, they might need an office receptionist to handle the schedule, or a partner to assist lifting heavy equipment. Perhaps they use a mechanic to ensure their vehicle is reliable and serviced regularly. Then they’ll need to put gas into that vehicle at a gas station and may stop to purchase lunch daily.

I’m sure you see where I’m headed. The housing market has long been shown to create an 11 times 11 times 11 positive ripple effect on the economy. Or maybe that was only known by me and a former coworker of mine. 😁 But now YOU know too! So in a very indirect way, perhaps the mortgage industry is killing off those murder hornets and meth gators!!

Let’s get serious about laughing now ...