Alternate title, “21 [Million] Questions”

Yeah, sorry Eugene. There are not so many enlightening questions in the mortgage industry right now. There are, however, LOTS of “Yikes!”

As the coronavirus rages through the country, every industry has been significantly disrupted. Let’s focus on that disruption in the mortgage business. But before we go there, it is our sincere hope that you and your loved ones are healthy and safe. And, yes, we will be adding some humor here (that is our role) and we want no one offended--ever. But I am one of those annoying people who needs to find humor in everything. So here we go.

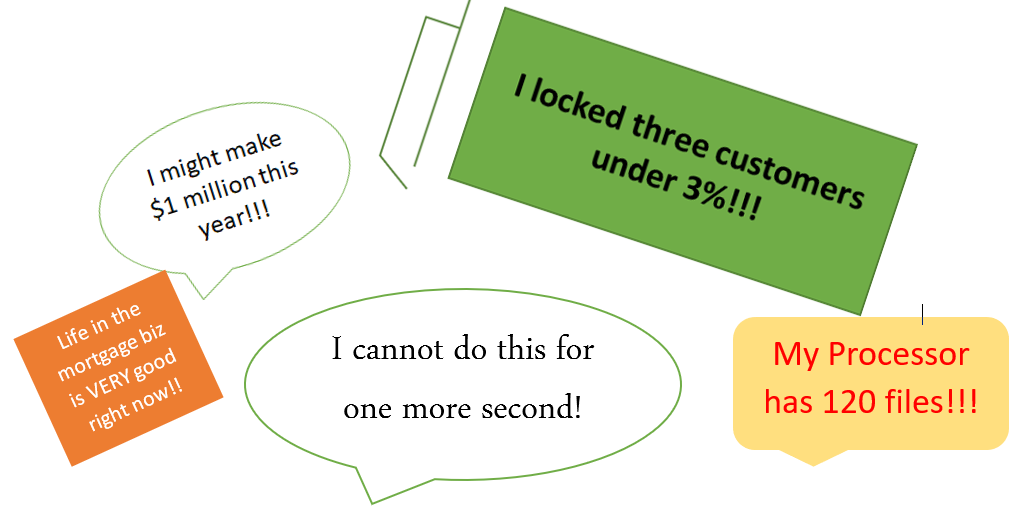

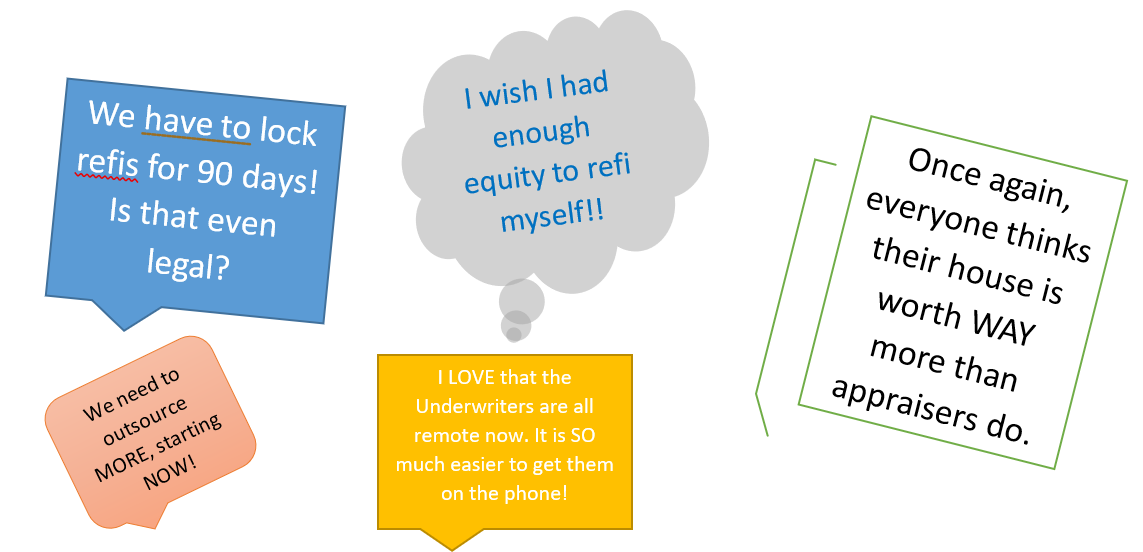

First and foremost, what’s happening inside home loan lenders nationally? To

determine that answer, I first contacted about a dozen field level industry

people. Here are some of their verbatim comments.

Yes, opinions, attitudes, and work climates are all over the place. But what about mortgage employers? And how is this affecting home loan customers?

Eerily similar to the meltdown years of ‘07 and ‘08, it depends on the day, the cash, the company, the attitude, and the loan. The questions are endless and the answers change rapidly. For example, one lending manager told me his company changed interest rates 12 times in ONE day. He said 80% of his team’s pipeline was “floating.” How can you even attempt to do the right things in terms of the company and the customer with those fluctuations? Communication is critical, but how, when and what should get communicated?

And that is mainly regarding new mortgage customers. How about those of us who have existing home loans? You’ve probably heard about skipping mortgage payments on some of the news shows. Let’s be careful out there.

Are we skipping payments or going into forbearance-- and do they count as early payment defaults? And, if so, will FNMA generate an automatic repurchase status on those? And what is the difference between deferral and forbearance? The answer just might depend on the lender. More here. But the most accurate response at the moment is, “We don’t really know yet.” As written in Forbes,

“Yet another feature of the federal government’s coronavirus stimulus package is struggling to work as intended.

This time, it’s the Coronavirus Aid, Relief, and Economic Security (CARES) Act’s provisions around mortgage forbearance. While the bill sought to alleviate the financial burden on homeowners by allowing them flexibility on mortgage payments, the measures have thus far been plagued by vagaries and confusion among lenders and borrowers alike.”

Moving focus back to ‘new’ home loan customers, what about qualifying income? If Joe Schmoe was making $100,000 a year as a chef and the restaurant is now closed, is Joe getting paid? If yes, for how long will Joe continue to get paid? Will the restaurant ever open again? If Joe is purchasing a house solo, is there any income we can use to qualify Joe? If Joe closed on a new home purchase right before the pandemic, does his lender have the right to request new employment verification post-closing? You guessed it. Every answer is, “It depends”

More than 7 Million Americans are currently unemployed and that is expected to rise. Lenders cannot and will not repeat pre-2007 ‘throw caution to the wind’ activities and are tightening their lending standards. That creates even more questions than answers right now.

Can home inspectors even get inside homes now? If not, now what? Remote inspections such as these?

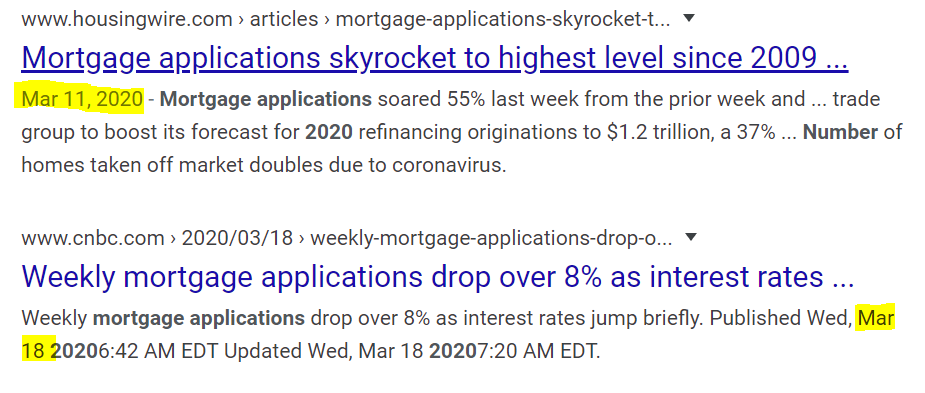

Then there is this from CNBC:

“Applications to refinance a home loan dropped 19% from the previous week but were 144% higher than a year ago.

Mortgage applications to purchase a home continued their sharp decline, falling 12% for the week and 33% year to year.”

But the week before, loan applications were at an all-time high.

What else is different, changing, or insane in the mortgage industry? Here are a few more things to ponder, summarized from HousingWire.

- Documentation: some lenders are dramatically reducing document “age” requirements, from 4 months to 2 months at Union Home Mortgage,for example.

- Verification of Employment is starting to get more challenging with HR staff working from home, employment in suspension, and standard IT tools possibly not available during the pandemic. United Wholesale Mortgage is now requiring an additional VOE check on the day of closing.

- US Bank and others increased minimum FICO requirements to 680.

Is that it? Not even close. Some lenders have essentially stopped taking Jumbo and Non-QM loans. Regarding the former, per Mortgage Professional America, “Wells Fargo has announced that it will drastically constrict its jumbo mortgage program amid the market turmoil caused by the COVID-19 outbreak.” Or, in the words of Bankrate, “Jumbo mortgage market disappearing as lenders shun risk.”

Then too, we must remember the rule of 11. When one house does not get purchased, 11 other industries suffer: moving, landscaping, home improvements, local food delivery, etc. So if you have stable employment (or sufficient cash), CAN/should you buy a new home right now? Once again, so many questions.

Will home sellers let people inside their homes during the epidemic? Do home sellers have someplace else to live or will that be a condition of sale? What if home sellers have the virus? What if home buyers have the virus? Will sellers allow you inside their home alone (as social distancing is required in mostly everywhere now)?

According to House Beautiful, “22% of respondents say sellers are taking their homes off the market in response to coronavirus concerns.” So do we wait or do we take advantage of incredible interest rates and buy? Like an earlier reply, that depends--on your finances, where you live, where you want to live, etc.

Regardless of your source of income, only one thing is critical right now--your health and the health of your loved ones. Since laughter is the best medicine, let’s see if we can administer some right now. I have over a hundred of these (no joke … pun intended). I’ll save some in case this horrendous virus sticks around.

Be well, stay healthy, keep laughing.

* I used to spin the toilet paper like I was on Wheel of Fortune. Now I turn it like I’m cracking a safe.

* I need to practice social distancing from . . . the refrigerator.

* Still haven’t decided where to go for Easter/Passover . . . The Living Room or The Bedroom.

* Every few days, try your jeans on just to make sure they fit. Pajamas will have you believe all is well in the kingdom.

* Homeschooling is going well. 2 students suspended for fighting and 1 teacher fired for drinking on the job!

* I don’t think anyone expected that when we changed the clocks we’d go from Standard Time to Twilight Zone.

* This morning I saw a neighbor talking to her cat. It was obvious she thought her cat understood her. I came into the house, told my dog . . . we laughed a lot.

* So, after this quarantine, will the producers of My 600 Pound life just find me or do I find them?

* Quarantine Day 5: Went to this restaurant called THE KITCHEN. You have to gather all the ingredients and make your own meal. I have no clue how this place is still in business!

* My body has absorbed so much soap and disinfectant lately that when I pee it cleans the toilet.

* I’m so excited . . . it’s time to take out the garbage. What to wear, what to wear?

* I hope the weather is good tomorrow for my trip to Puerto Backyardia. I’m getting tired of Los Livingroomia.