According to wordhippo.com, the opposite of hard can be any of the adjectives shown below.

Since it's fairly unanimous that last year was hard on many levels, I suggest we opt for the opposite. So facile it is. 👍

To attempt to determine whether or not that’s possible, let’s take a glimpse of the future. We can start by delving into “10 outrageous 2021 predictions for the mortgage industry” from National Mortgage News. In short, here are their crazy times guesses.

- Home values will go down and bubbles will form. Therefore, lending will become more conservative and revert to 20% down requirements for super strong borrowers with top credit and with financial reserves.

- “Twenty-five percent of all mortgages (mainly in cities like Austin, San Francisco and Denver) will be made in Bitcoin (BTC).”

- Lenders will change the way they assess borrowers because of the coronavirus. Lenders may require evidence of good health and having received the corona vaccine (to determine higher probability of continued employment and ability to repay).

- Social media content may affect loan approval using predictive algorithms based on your postings. [I must digress on this one and add … YIKES.]

- Tesla will start experimenting with creating smart manufactured homes.

- Amazon will offer super low cost title insurance.

- Rates may drop below 2%. [Good grief, will there be another refi boom?!]

- Mortgage industry scrutiny will increase tremendously.

- Non QM loans will not increase.

- Liquidity in mortgage servicing rights will climb

- Our friends at Rocket [Mortgage] will explode a tech space race in the third party origination side of the business.

- FHA will lower UFMIP and even allow for the end of monthly MI

- Correspondent jumbo mortgages will become part of a price war.

- Home equity loans will be back.

- Non-QM loans will increase dramatically. [Yes, this contradicts a bullet just above. The crystal ball is blurry!]

- "Values of publicly traded mortgage companies will fall by 50% as investors fear a decade of weak refinance activity and its negative impacts on independent mortgage bankers' net income," said Daniel Jacobs, Tru Loan Mortgage managing direct.

- Tweets will not impact regulatory policy!

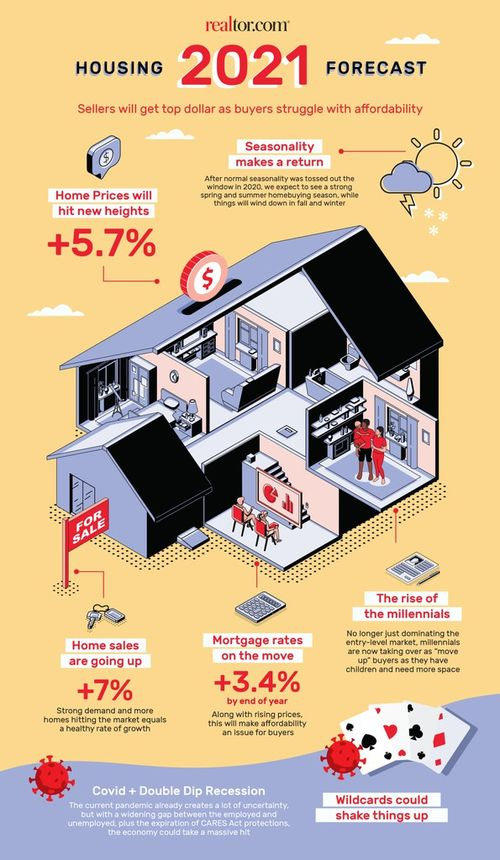

Unlike in previous years, I did not make this stuff up! Woo hoo! But it seems that others have jumped on the prediction bandwagon as well. Here’s what Realtor.com thinks.

- Home price growth will slow from double digits to 5.7%.

- Mortgage rates will rise to 3.4% by year end.

- Sales of existing homes will increase 7% with many people “up-sizing” and/or seeking new amenities (like pools) due to being stuck at home.

- More homes will be for sale based on builder completions and new listings.

- The wild cards in all of these, of course, include covid and the economy.

Next let’s continue the fun with some “flip side” commentary.

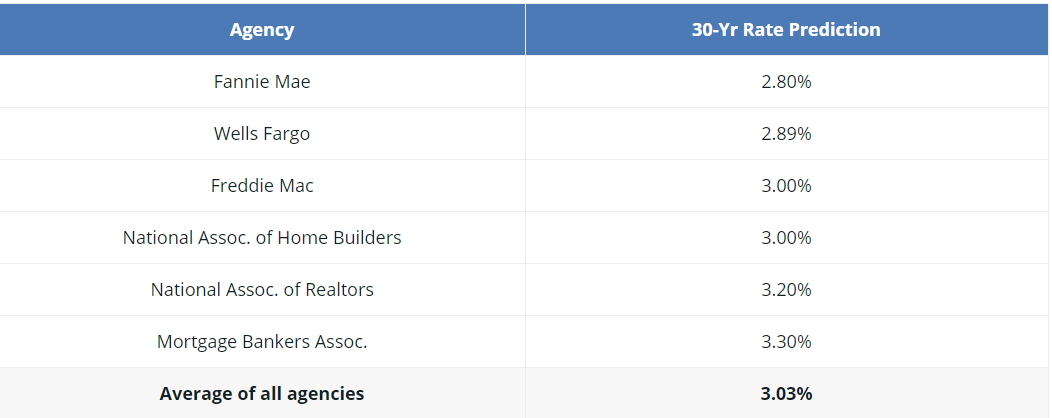

Mortgage Reports posted this interest rate chart:

While not “all over the board,” it does not seem to agree with the earlier prediction of under 2%.

Msn.com reports that the Mortgage Bankers Association and Freddie Mac both predict home prices to increase in the range of 2%. That’s a tad less robust than Realtor.com. CoreLogic comes in even more conservatively at a 0.2% increase.

Finally, let’s take a glimpse at one more view through the looking glass, courtesy of nerdwallet.com in “The Property Line: 8 Housing and Mortgage Trends for 2021.”

- Rates may keep falling … a bit.

- Home sales and costs will keep rising.

- Housing Counselors will be in demand as homeowners in forbearance are more likely to speak with them than their mortgage companies.

- Renters may be evicted. Landlords are owed up to $34 Billion.

- Well paid buyers will be buying homes; service industry employees will likely not.

- Black households are likely to be disproportionately harmed in 2021.

- Suburbs will grow but many cities will go in an opposite direction.

- The Ability to Repay rules may be scrapped or revised.

So what does all of this mean? In the words of baseball’s great Casey Stengel, “Never make predictions, especially about the future.” 😆

But let’s do that anyway! We’ll add the same disclaimers and “unless” clauses and blah, blah as everyone else. Here we go with our top 5:

- Industry leaders partner to create and sell homes on the moon, built by Pulte, with solar power courtesy of Tesla, financed by Rocket Mortgage. They’ll be called PuTeR Homes, No Gardens.

- In order to lock in a mortgage interest rate, borrower(s) will need to join an online odds maker site such as OddsMaker.ag or OddsOnline to be available on ratezip.com.

- The state of New York will pay anyone a $10,000 “Please” bonus to move into the state.

- Similarly, the state of Idaho will pay a $10,000 “No!” bonus to people who choose not to move into the state.

- Essential workers, including nurses, waitresses, waiters, employees of Home Depot, Lowe’s, WalMart, and the post office etc., will be able to buy homes with mortgages at 1% that require no underwriting review.

So what are your predictions for the 2021 mortgage industry? Did I hear, “It will make me laugh?” Well then let’s get started on that immediately.

What do you call a woman who sets her mortgage documents on fire?

Bernadette

Why was the mortgage so clingy?

It hated being alone.

The loan officer approved my plan to go forward and take out a mortgage for the horse farm I've been looking at.

He called it a stable investment.

Why couldn't Spongebob refi?

Because his house was underwater.

I'd like to take a moment to say thank you student loans for getting me through college.

I don't think I'll ever be able to repay you.

How to rescue the economy:

Dear Mr. President,

I believe we need to require patriotic retirement. There are about 40 million people over 50 in the workforce. Pay them $1 million a piece severance with stipulations:

1) They must leave their jobs. Forty million job openings = Unemployment fixed!

2) They must buy NEW American cars. Forty million cars ordered = Auto Industry fixed.

3) They either buy a house or pay off their mortgage = Housing Crisis

fixed.

All this and it's still cheaper than any "bailout". 😜