For What?

It appears that those in real estate and the world of home financing may soon be granted their #1 Wish? Yes, Millennials are buying houses! What has stopped them, other than huge student loan debt, lack of affordable housing inventory, and super accommodating parents?

In USNEWS, we discover that millennials can hold several misconceptions about home buying. They think their credit scores are too low. They think they need a 20% down payment. They think they need a lot of established credit. But the truth is their average credit score is higher than the lowest acceptable score (or around 580), they can buy a home with as little as 3% down, and the new credit scoring model might be perfect for them. As told by Yahoo Finance:

“... the launch of the UltraFICO Score later this year could be a game-changer for millennials with low scores because of a limited credit history, Loomie says. The credit scoring model will allow mortgage applicants who don't initially qualify for a loan to opt into having bank account data used to further gauge their creditworthiness. UltraFICO offers a revised score based on factors such as average account balance and automatic deposits from payroll or other sources.”

Digression alert! Dave Ramsey made and lost millions of dollars. In 1992, he formed Ramsey Solutions to help those who were hurting from the results of financial stress. He’s written books and has a radio call-in show called The Money Game, now nationally syndicated as The Dave Ramsey Show.

Regarding UltraFICO, Dave calls it Ultra Ridiculous. He hates credit scores and mostly everything about them and believes, “... it’s really just a score of how well you can play the debt game with the bank.”

Ultra Fico uses algorithms containing how long your bank accounts have been open (checking, savings and money market) and your activity in them. Do you have overdrafts? How many, how often? Do you have direct deposits from your paycheck? Do you add money to savings and leave it there?

You have to have at least $400 in your account. Using this new method might add about 20 points to your FICO score. That means you might be able to borrow more, or more easily. Dave thinks the entire premise is, “... sleazy. It’s shoddy. It’s sketchy. It’s just plain bad.”

But many banskers think UltarFICO will be of great assistance to Millennials with thin credit. And once that group gets past their misconceptions, raises their FICO, and feels ‘ready,’ how do they start the homebuying process? It should come as no surprise, they start with the Internet. And that’s not just sitting behind a computer at home or work. Per Keller Williams:

“The NAR has said that 94% of Millennial home buyers start by looking at online listings. They list high-quality photos (and even video presentations) to be crucial when considering a listing. And this isn’t only from a desktop computer…over half of Millennial buyers start this process on a mobile device, and half of those buyers end up finding their home through that mobile device!”

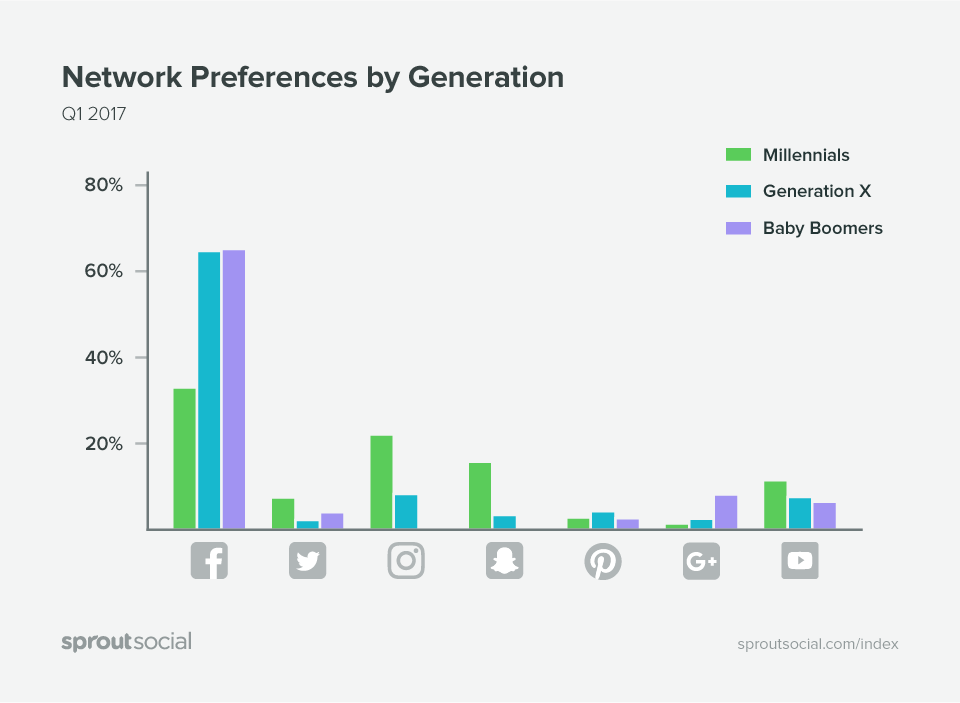

Once they find that house, they use tools like ratezip.com, rocketmortgage.com, or a different online mortgage lender. And, of course, they also use social media to check into the neighborhood, public transportation, nearby friends and relatives and all things related to housing. Here’s what they check most often, per businessgrow.com.

Who?

From Forbes, “Yes, Millennials Really Are Buying Homes. Here’s How.”, we learn that the homeownership gap where Millennials are concerned still exists, but they are buying. Only 32% of Millennials own homes versus older generations--60% for Gen X and 75% for Baby Boomers. And the race and socioeconomic differences still exist.

“Who is the Millennial buyer? They are disproportionately married. They are disproportionately well educated and more affluent. They are disproportionately white,” says Laurie Goodman, co-director of the Housing Finance Policy Center at the Urban Institute.

Goodman’s research shows that marriage is the single biggest predictor of whether a Millennial owns a home, with matrimony increasing the probability of being an owner by 18 percentage points. Having a child increases the likelihood of owning a home by 6.2 percentage points, and having a parent who owned a home increases someone’s probability of owning by 10.9 percentage points.”

So wealthy, white, married millennials with a child and with a parent who owned/owns a home are buying homes. Is that horrendous? Or is it a start?

WHERE?

As reported by Boston.com and by others, “A national trend shifts. More millennials are buying homes in the burbs.” So the walk to Starbucks, the Uber ride to the show, and meeting friends at the museum days may be going away?

I live in the burbs and my neighbors were shocked when a young couple from the City with two young boys and two sets of suburban home owning parents recently bought a place on our street. Their biggest complaint is that there are no other young kids on the street and ‘not much to do here.’ Part of that appears to be ‘yet.’ Since they moved in, 4 more homes are for sale on my street. I’d say the odds of youth coming ‘home’ soon here is now quite high. And literally every weekend, one set of parents or the other are at their house blowing leaves, decorating, bringing supplies, etc. Maybe Millennials moved out of their parents’ basements and now the parents stay part time in the millennials basements? Ah, the Circle of Life.

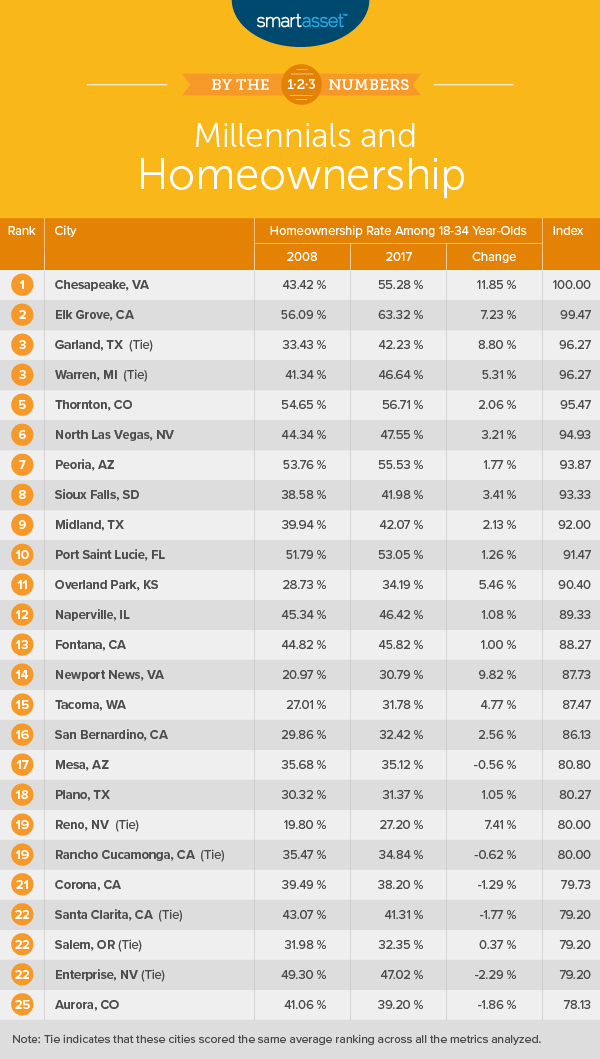

For more on Where?, check this out from smartasset.com.

WHY?

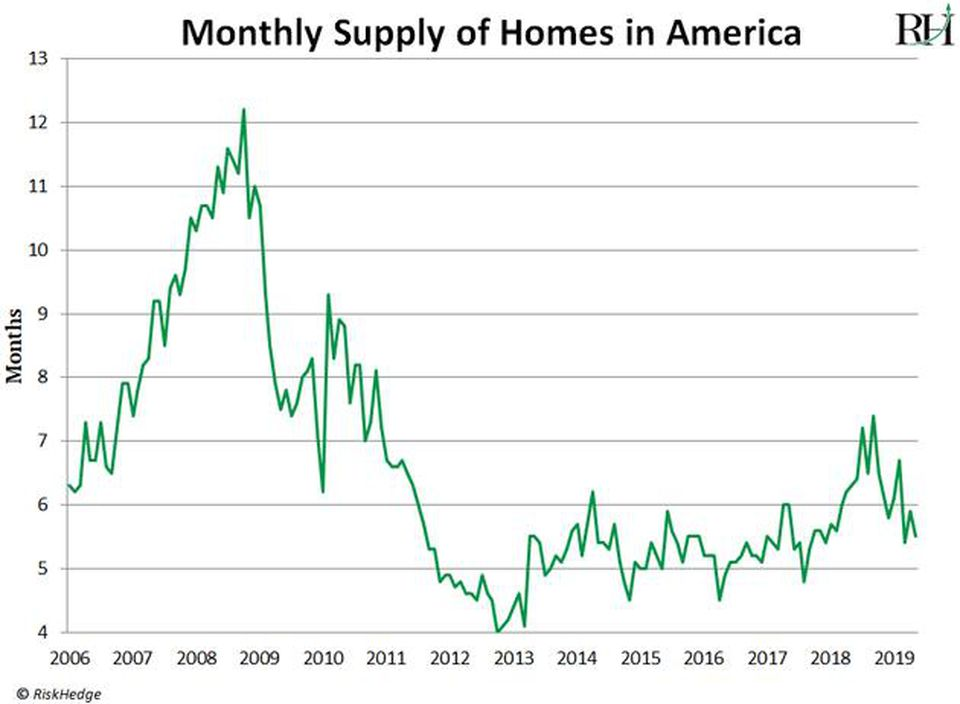

According to Forbes magazine, “The Biggest Housing Boom In History Has Just Begun.” It is and has been a supply and demand issue, illustrated here.

Calling?

According to Housing Wire More first-time homebuyers enlisting help from family, friends. Specifically, “The 2019 Profile of Home Buyers and Sellers report from the National Association of Realtors revealed that more than 30% of first-time homebuyers used down payment help from family and friends.”

My father used to call it, ‘The bank of dad.” Funny thing is, the hours were minimal and the funds were extremely difficult to obtain. I think my father loved me but he had a unique perspective on life and money. He would often say, “It’s my money, I earned it, and worked hard for every penny. You should do the same. You’re more than capable.” He lived every day to the fullest and spent nearly every penny he had. Good for him and I have no hard feelings. He could never, however, have parented a typical media portrayed millennial. 😬

All’s Well?

Well, not exactly. In terms of millennials and home buying, and according to CNBCs, “63% of millennials who bought homes have regrets—usually because they missed this one crucial step.” That critical missing piece was the planning ahead for maintenance, repairs and other hidden costs. Those unforeseen expenses can include insurance, property taxes, initial closing costs, condo assessments, furniture, desired electrical upgrades, etc. Holy avocado toast!

But let’s not end with a 😒. Instead, let’s have some fun!

So there!!