Time to Refi?

This is not an old blog!

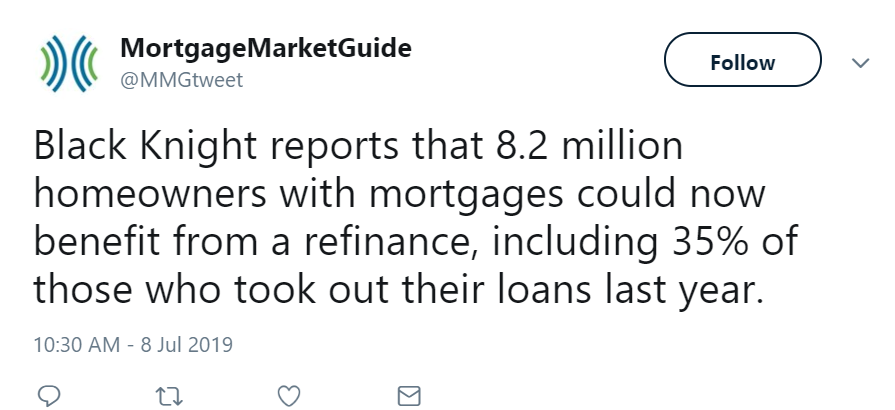

Check out this Tweet, especially the date!

According to themselves, Mortgage

Market Guide is “The most reliable source of information available

to protect your pipeline and help your clients make sound decisions.” Black

Knight “(NYSE:BKI) is a leading provider of integrated software,

data and analytics solutions that facilitate and automate many of the

business processes across the homeownership life cycle.” So that’s the

opinion of two highly regarded expert solutions companies available to

mortgage professionals. What does everyone else think?

UMassFive, the college federal credit union, says maybe. They recognize rates are low again and advise people to review their finances and current mortgage interest rate. Next, they should estimate how much longer they plan to stay in their homes.

Investopedia has similar thoughts but for somewhat different reasons. Their rationale has more to do with building equity by making different payments--for a shorter term or at a lower rate or at a fixed versus variable rate.

AARP

chimed in and alluded to the fact that a cash out refi might just easily

supply funds to people 15 or more years from retirement. Also noted were

suggestions to keep things reasonable, have a back up plan, to make a long

term plan and to earmark a specific plan for the funds.

Let’s compose a short summary by listing the Pros and Cons of a mortgage

refinance. Here’s the beginning of a chart you can use.

| PROS | CONS | ||

| Lower monthly payments yield more disposable income. | Yes, but what is your plan for that extra cash—investment, home improvement, a college fund …? Make sure your plan is better than, “waste it!” | Refinancing adds more years until the loan is paid off. | But wait, consider a 15-year fixed if you had a thirty year. Or consider retirement, upsizing, downsizing—will you sell this house before the loan is paid? |

| Application process may now be fast and easy | Good credit? Plenty of equity? Assets in shape? Job history smooth and lengthy? Consider using an online, expedited site for a fast and easy process. | Application process may be lengthy | Prepare in advance! There are plenty of sites to help you do that (like this) and there are loads of mortgage professionals who will give you a pre-qual or pre-approval or at least a list of items needed. |

| You may be able to do this with little or no upfront costs. | There are loads of “no cost” refis available – again. | There may be upfront costs | If you pay points up front, your rate and, therefore, the monthly payment is even lower! |

| It is possible you can take cash out and complete home repairs, payoff bills, etc. | If your rate is lower and you have equity, you might be able to get a lot of cash and still pay a lower rate each month! | You may not have sufficient equity to take cash out. | You may still be able to refinance! Here’s just one possibility. |

| Rates may go higher soon. | No one has a working crystal ball. | Rates may still drop. | No one has a working crystal ball. |

| Then there’s this …. | 8 reasons to refinance your mortgage | Then there’s this …. | 7 Bad Reasons to Refinance Your Mortgage |

Unless you choose a lender who offers a “reduced documentation” refi option,

you will need to provide seven categories of paperwork,

according to MortgageLoan.com.

In general, you will have to:

1) Prove your income via paystubs, tax returns, W-2s, 1099s--whatever is applicable.

2) Supply paperwork for all kinds of insurance including homeowners, condo association, title, and other applicable insurance (like flood).

3) Know the details of your credit report/score (but check that the right way). Normally your lender will supply this documentation, but it is often a good idea to check out your credit score in advance, as mistakes happen.

4) Verification of all debts including alimony, child support, current mortgage payment (and home equity lines if applicable), credit cards, car loans, student loans, etc.

5) Document all of your financial assets other than your home. This means checking and savings accounts, stocks/bonds, mutual funds, CDs, retirement accounts, other real estate, and your Louboutin shoe collection (joking about that last one … in most cases).

6) Estimate your home value. All calculations for the refi will be based on this value. Your lender will most likely have an appraisal done which will substantiate your guess (or not). Consider checking out recent homes sales in your neighborhood where the properties were similar to yours to make an educated guess at value. Also be ready to document significant home improvements since the purchase. That might include an addition, extensive bath or kitchen remodeling, etc. Do not be surprised when that $50,000 pool, deck and porch renovation do not make your house worth $1 more than others without those luxuries. Some buyers want pools filled in before closing, really.

An additional “next step” that is wise is to use a Mortgage Refinance

Calculator. There are oodles of them available online. Just check out this

search done on DuckDuckGo. Time for the standard

digression.

For those of you who are not up on internet searches, Big Brother really IS

watching. In other words, did you ever decide to buy a gift for your brother

in law of a Velvet

Elvis and then noticed those goofy things appear as side bars for

the next week, regardless what you sought online? If that kind of personal

tracking of your bizarre tastes bothers you, an option is to use DuckDuckGo

(and similar search engines) instead.

Here’s their philosophy. “We don’t store your personal information. Ever. Our

privacy policy is simple: we don’t collect or share any of your personal

information.” That means no one at DuckDuckGo cares about Velvet Elvis and

you’ll never see them appear as ads on your other searches!

According to Hongkiat, here are 12 search engines that do not track (that are “private”).

- DuckDuckGo

- WolframAlpha

- Startpage

- Privatelee

- Yippy

- Hulbee

- Gibiru

- Disconnect Search

- Lukol

- MetaGer

- Gigablast

- Oscobo

Digression complete. Back to topic. Perhaps then, it is time

to refi your mortgage. And if you’re still asking, “How will I Know,”

don’t take Whitney Houston’s advice. Instead, shop the rates first. You can

do that right here at RateZip!

Read more at:

Should I refinance? Reduce your interest rate with 2019‘s low rates

When

Mortgage Rates Are Low, It's Always A Good Idea To Refinance, Right?

Not Necessarily.

Did you hear about the Mortgage Enthusiast Club? They had to disband due to lack of interest.

What happened when the man couldn't afford the mortgage on his haunted house? ...it was repossessed!

Why couldn't Spongebob refinance his mortgage? Because his house was underwater.

How did the bag of fertilizer help the vegetable farmer pay his mortgage? It raised his celery…

What was the mortgage afraid of? Dying a loan.