Is Polonius Full of Balonious?

From literary devices, in Act-I, Scene-III of William Shakespeare’s play, Hamlet, Polonius counsels his son Laertes before he embarks on his visit to Paris. “He says, “Neither a borrower nor a lender be; / For loan oft loses both itself and friend.” It means do not lend or borrow money from a friend, because if you do so, you will lose both your friend and your money. If you lend, he will avoid paying back, and if you borrow you will fall out of your savings, as you turn into a spendthrift, and face humiliation.”

Let me next quote another literary giant (joke!) P.T. Barnum, who once said, “There is scarcely anything that drags a person down like debt.”

Suppose you had the chance to pull that person up? Would you take that chance? What if the person was your mother, father, sister, brother, best friend, … would that make a difference?

No, no, these are not Jack Handey Deep Thoughts from SNL. (But if you click that link, there are some classics posted there). Today’s blog is food for thought, ideas for the fertile mind to ponder, points of discussion, an offer for readers to pay all my debt … you pick!

Outdo Mom and Dad?

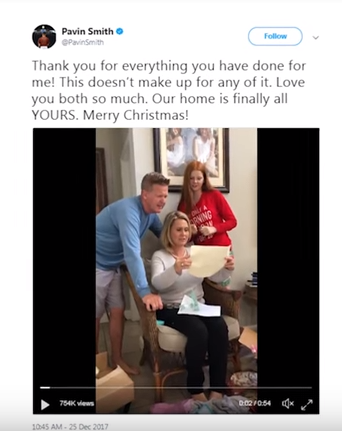

My dad used to often tell me that his favorite dream was that his kids did better in life than he did. Many parents must feel the same and are now be rejoicing that it has apparently happened, often in big ways. Look at this documentation of that.

Pavin Smith is a Major League Baseball prospect. He got a $5Million dollar bonus for signing. Look what he did with part of it and posted on Twitter, as seen on YouTube! He paid off his parent’s mortgage!

The Road to Hell or Florida?

Many years ago, I had a job that paid very well and I also got a bonus (but clearly not for my athletic prowess, ha). At that time, my parents were following the ‘senior law’ and spending 3 months every year in Florida (and the rest of the time in Pennsylvania). When they traveled to Florida, they spent a month in a hotel and then two weeks with my uncle, my cousin, my mother’s friend, and another relative. That worked for them, but it was not ideal.

So my husband and I used my bonus to buy them the house next door to my uncle in Fort Myers, FL. They were thrilled! Of course, it all backfired when they decided to sell their Pennsylvania house and move permanently to Florida and visiting them because a cumbersome flight versus a two hour drive. Oh well ... the road to hell and all that ... 😈

But let’s go back to paying off parents’ mortgages. It's a fabulous idea, isn’t it? Of course it is! Let’s examine this a bit …

How Much Will This REALLY Cost me?

According to a Reddit blog, each child and his/her spouse can “gift” each parent $15,000 per year without reporting it! So if there are three children and all are married, and one mother and one father, then 6 people (the child + spouse) can gift a total of $30,000 ($15,000 to mom and $15,000 to dad) times six or $180,000! Or, if that doesn’t work, the givers can make it part of their gift and inheritance exemption of $5.6 million. Gift taxes don't apply until the gifter has given over $5.6 million per person.

Suppose you have no siblings and are unmarried. Not to worry! A child can still gift parents the amount needed to payoff an average mortgage in its entirety, report the amount over the allowable $15,000 and and file form 709 and simply deduct it from that aforementioned lifetime exclusion.

If a child knows the mortgage account number, payment address, etc. s/he can make the payment directly to the collector, as long as the account number is included with the payment.

Since mortgage payments normally include taxes and insurance, can the child declare those when filing income taxes? Well, no. To deduct mortgage interest on taxes, the person must be legally liable for the debt and have documented ownership in the home.

Wiki, not Waikiki

Now, lovely readers, I am already anticipating your next question. Can you pay off a mortgage of a person who is not your parent, child or relative? And, yes of course, feel free to payoff mine. Would you like to know how to do that? Once again, the awesome Internet provides us with a Wikihow entitled, “How to Pay off Someone Else's Mortgage.” How great is that?

Never Assume?

In addition to all described above (simply substitute your name for “child”, tee hee), you can also often “assume” a mortgage belonging to someone else. This method requires you to “own” the debt officially. That’s good in that you can then write off the interest, but maybe less good since making all future payments lands firmly and squarely on your shoulders.

Note that not all mortgages can be assumed. FHA and VA loans are, but that is not always the case with conventional financing. Further, not all people will be able to assume a mortgage. There are credit requirements and possible affordability criteria (especially if the interest rate changes). The lender may also have a “due on sale” clause in the original mortgage which they may not be willing to waive. In that case, the interested party may need to apply for a new mortgage completely.

“I just miss - I miss being anonymous.” ~ Barack Obama

Or, you can arrange to make an anonymous mortgage payment (or two or three or …). To do this, you’ll need the property title (viewable at the County Recorder's Office in the county where the property is located) and the name of the lender. Title examiners can often be hired to do this work for you. Then send a money order to the lender and include the property address (and account number if you are able to find that).

But if the need for anonymity is not present, a person can opt to simply make the mortgage payments for someone else. Suppose you know someone who has a mortgage payment of $1200/month (who obviously does not live in NJ, NY, or CT ... sorry, little joke). If one person decided to make all of those payments, that’s $14,400 in a year, less than the 2018 exemption of $15,000 annually. There is, then, no gift liability.

Stealing a phrase from many, “It’s all good!”. Correct? Well, maybe not ALL. In AsktheMoneyCoach.com, I found “The Pros and Cons of Paying Off Someone Else’s Debt.” And, to be clear, this thinking is reversed depending on whether you are the “Payer” or the “Lucky Dog Recipient.”

Here are the Pros:

- Assisting a person or person who has suffered a setback or needs to stay afloat.

- Giving someone a fresh start.

- Helping someone qualify for larger financing.

- Feeling like you hold a magic wand or have achieved sainthood (Sorry! I made that last one up; it’s NOT in the article!)

But with all those obviously positive reasons to do something fantastic for another human being, first consider the Cons.

Taking a risk with your own credit and finances.

For example, if you cosign a loan and the other party pulls a Snaggelpuss and makes an exit, stage left, you are holding the bag (or the house, as the case may be). Not only will this drain your finances, it could smear your credit in a big way also.

And if you take a loan from a retirement account to obtain the money, you may have to pay early withdrawal fees and taxes on what you took out, and that doesn’t include the investment potential of the money you withdraw.

Serving as the Enabler

If the person you assist has a history of chronic money problems, is your help really serving to solve the problem? Is gifting this person cash helping them positively change their behavior? And if you loan the money with an understanding it will be paid back, is that realistic? And what if it is not paid back or paid on time?

Adversely affect the relationship

Will you consciously or subconsciously resent the person to whom you gave money>> Will they feel that way about you? How will your spouse or partner feel about you giving (or receiving) money from a friend or relative? And, for certain, you need to tell him or her.

And don’t get me started on the number of hideous romance novels out there where Party A is dating Party B and loans him or her a boat load of money and never sees that or the Party again! Yep, the party's over! (Sorry, couldn’t resist.)

Never lend money to a friend. It's dangerous. It could damage his

memory.

- Sam Levenson

Q: What does one penny say to the other penny?

A: Let's get together and make some cents.

“The safest way to double your money is to fold it over and put it in your pocket.”

` Kin Hubbard